Cashless vs Reimbursement Travel Insurance: What’s the Difference?

26 Jun. 2026

A travel insurance claim does not always work the same way for every medical situation. In some cases, the hospital may coordinate directly with the insurance company. In others, the traveller may need to pay the bill first and claim reimbursement later.

That difference matters, especially during international travel, where medical costs can be high and hospital billing systems may not be familiar. Cashless travel insurance, or direct billing, can reduce upfront payment when it is available. Reimbursement gives travellers a way to claim eligible expenses after paying for treatment, but it depends heavily on proper documentation.

Understanding both options before travel can help families avoid confusion during an emergency. This blog explains how cashless and reimbursement claims work, their key differences, and which option may be better in different travel situations.

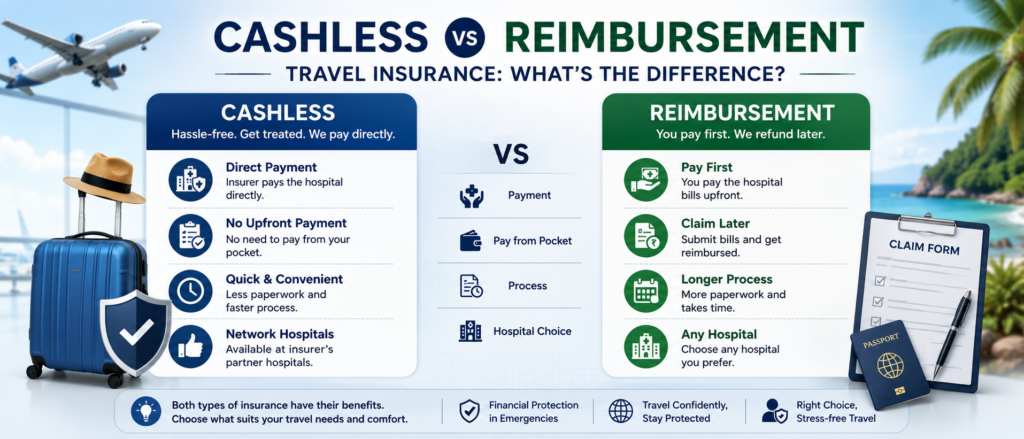

Cashless or Reimbursement Travel Insurance?

In cashless travel insurance, the hospital or medical provider may send the bill directly to the insurance company for eligible expenses. This is often called direct billing in travel medical or visitor insurance. In reimbursement travel insurance, the traveller pays first and submits the claim later with bills, receipts, medical records, and other documents.

Cashless is usually more convenient when it is available. On the other hand, reimbursement gives more flexibility but requires the traveller to manage upfront payment and paperwork.

What Is Cashless Travel Insurance?

Cashless travel insurance means eligible medical expenses may be settled directly between the medical provider and the insurance company. The traveller may not need to pay the full bill upfront, although deductibles, co-payments, non-covered expenses, or excluded items may still need to be paid separately.

For international travel insurance, especially visitor insurance for the USA, this is often referred to as direct billing. The hospital, clinic, or healthcare provider sends the bill to the insurance company or claims administrator. The insurer then reviews the claim based on the policy terms.

However, cashless does not mean automatic approval. The treatment must be covered under the policy, the provider must be willing to bill the insurer directly, and the required process must be followed. In many cases, contacting the insurance assistance team early can make the process smoother.

What Is Reimbursement Travel Insurance?

Reimbursement travel insurance works on a pay-first, claim-later basis. The traveller pays the medical bill at the hospital, clinic, pharmacy, or doctor’s office and then submits a claim to the insurance company.

The claim usually requires supporting documents such as itemized bills, payment receipts, diagnosis details, prescriptions, medical records, and a completed claim form. The insurer reviews the documents and reimburses eligible expenses as per the policy terms.

This option may be useful when the traveller visits a provider that does not offer direct billing, when treatment is taken outside the network, or when the expense is smaller and easier to pay upfront.

Cashless vs Reimbursement Travel Insurance

| Point | Cashless / Direct Billing | Reimbursement |

| Who pays first? | The provider may bill the insurer directly | The traveller pays first |

| Upfront payment | Usually lower, but deductibles or non-covered costs may apply | Usually higher because the traveller pays the bill first |

| Best suited for | Hospitalisation, emergency care, high medical bills | Doctor visits, pharmacy bills, smaller claims, non-network providers |

| Provider role | Provider must agree to direct billing | Provider only gives treatment and documents |

| Documentation | Still required, but provider may send part of the bill directly | Traveller must collect and submit all documents |

| Main benefit | Reduces immediate financial pressure | Offers more flexibility |

| Main limitation | Not guaranteed everywhere | Requires funds and proper paperwork |

How the Cashless Claim Process Usually Works

The exact process can vary by insurer, but it generally follows this flow:

- The traveller contacts the insurance assistance team or claims administrator.

- The insurer guides them to a network or suitable medical provider, if available.

- The traveller shows the insurance card, policy details, and ID proof.

- The hospital or provider confirms whether direct billing is possible.

- The provider sends billing details or a request to the insurer.

- The insurer reviews the treatment against the policy terms.

- Eligible expenses are settled directly with the provider.

Even with cashless treatment, the traveller may still need to pay the deductible, co-insurance, uncovered services, or expenses beyond policy limits. Direct billing only applies to eligible expenses under the plan.

How the Reimbursement Claim Process Usually Works

In a reimbursement claim, the traveller has to be more careful with documentation. The basic process includes:

- Get the required medical treatment.

- Pay the hospital, clinic, doctor, or pharmacy bill.

- Collect itemized bills, receipts, prescriptions, and medical reports.

- Complete the claim form.

- Submit all documents to the insurance company or claims administrator.

- Wait for claim review.

- Receive reimbursement for approved eligible expenses.

The most common reason reimbursement claims become stressful is missing paperwork. A simple receipt may not be enough. Insurers often need itemized bills, diagnosis details, proof of payment, and medical records to understand whether the expense is covered.

Which Is Better: Cashless or Reimbursement Travel Insurance?

Cashless is usually better when the medical bill is large, especially in countries where healthcare costs are high. It can reduce the immediate financial burden on the traveller and their family. This is why many people prefer plans with network access or direct billing support.

Reimbursement may be better when the traveller wants flexibility in choosing a provider or when the medical facility does not support direct billing. It can also be common for smaller expenses, such as clinic visits, medicines, diagnostic tests, or follow-up care.

The better option depends on the situation. For emergency hospitalisation, cashless or direct billing can be very helpful. For smaller or non-network expenses, reimbursement may be more realistic.

What Travellers Should Check Before Buying a Plan

Before choosing travel insurance, it helps to check a few claim-related details:

- Does the plan support direct billing or cashless treatment?

- Is there a provider network in the destination country?

- What is the deductible?

- Does the plan include co-insurance?

- Are pre-existing conditions covered or excluded?

- What documents are required for reimbursement?

- Is pre-authorisation needed for hospitalisation?

- How quickly should the insurer be informed during a medical emergency?

These details matter because the claim experience depends not only on the policy maximum but also on how the claim is handled when treatment is needed.

Common Mistakes to Avoid During a Claim

Many claim delays happen because travellers assume the process will be automatic. It usually is not.

Avoid these common mistakes:

- Not contacting the insurer or assistance team early

- Assuming every hospital will accept cashless billing

- Not keeping itemized bills and receipts

- Losing prescriptions or medical reports

- Paying the bill without asking if direct billing is possible

- Waiting too long to file the claim

- Assuming all medical expenses are covered

A little preparation before the trip can make the claim process easier later.

How OnshoreKare Can Help

Choosing travel insurance is not only about comparing premium amounts. It is also about understanding how the plan may work during a real medical situation abroad.

OnshoreKare helps travellers compare visitor insurance plans based on coverage, policy maximum, deductible, network access, pre-existing condition benefits, and claim support. If you are buying insurance for parents, relatives, or yourself, it helps to understand the claim process before the trip begins.

Compare travel insurance plans with OnshoreKare and choose a policy that matches your destination, health needs, and budget.

FAQs

Is cashless travel insurance guaranteed at every hospital?

No. Cashless or direct billing depends on the provider, insurer, network availability, and policy terms. Some hospitals may still ask the traveller to pay upfront and file for reimbursement later.

Does cashless mean I pay nothing?

Not always. You may still need to pay deductibles, co-payments, non-covered expenses, or charges beyond the policy limit.

How does reimbursement work in travel insurance?

The traveller pays the medical bill first, collects all required documents, and submits a claim to the insurance company. The insurer reviews the claim and reimburses approved eligible expenses.

Which is better for international travel?

Cashless is usually more convenient for large medical bills or hospitalisation. Reimbursement is useful when direct billing is not available or when the traveller visits a non-network provider.

What documents are needed for reimbursement claims?

Common documents include claim forms, itemized bills, payment receipts, prescriptions, diagnosis details, medical reports, and proof of insurance. The exact list can vary by insurer.